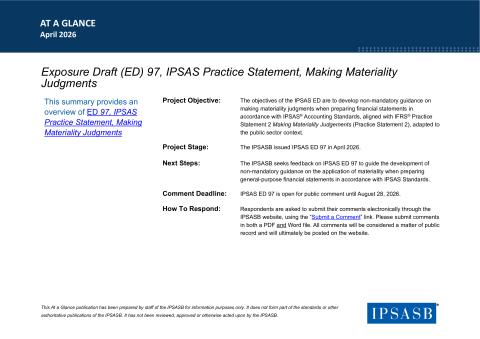

Exposure Draft (ED) 97, IPSAS Practice Statement, Making Materiality Judgments

The objectives of the ED 97 are to develop non-mandatory guidance on making materiality judgments when preparing financial statements in accordance with IPSAS® Accounting Standards, aligned with IFRS® Practice Statement 2 Making Materiality Judgements (Practice Statement 2), adapted to the public sector context.

Comment by August 28, 2026 in English.

Copyright © 2026 The International Federation of Accountants (IFAC). All rights reserved.