Image

The IPSASB develops accounting and sustainability standards for use by public sector entities. The structures and processes that support the operations of the IPSASB are facilitated by the International Federation of Accountants (IFAC). The IPSASB’s Strategic Objective is:

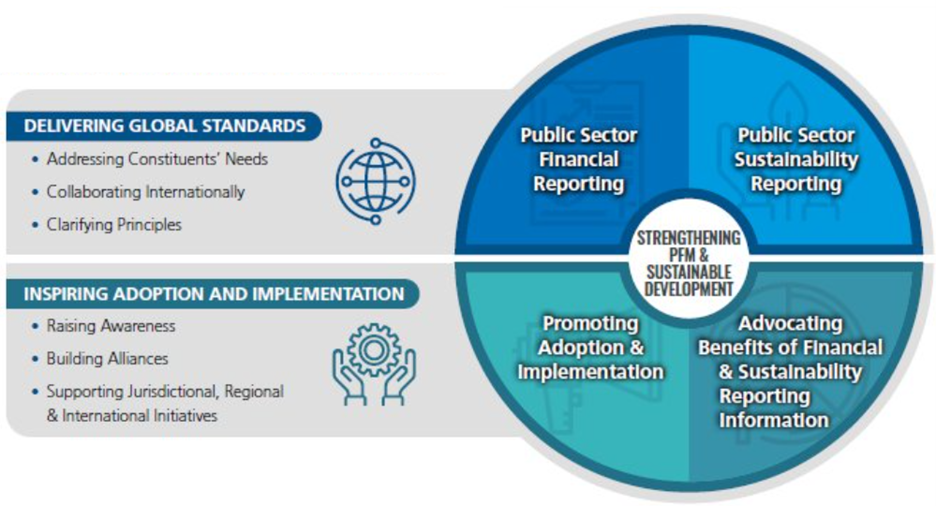

Strengthening Public Financial Management (PFM) and sustainable development globally through increasing adoption and implementation of accrual-based International Public Sector Accounting Standards® (IPSAS®) and IPSASB Sustainability Reporting StandardsTM (IPSASB SRSTM).

The strategic objective is delivered through two main areas of activity, both of which have a public interest focus:

- Delivering Global Standards. Developing and maintaining public sector financial and sustainability reporting standards; and

- Inspiring Adoption and Implementation. Raising awareness of the IPSASB Standards and the benefits of their adoption and implementation.

The IPSASB follows an open and transparent due process to ensure that IPSAS and IPSASB SRS are developed in the public interest. This process provides the opportunity for all those interested in public sector financial and sustainability reporting, including those directly affected by the Standards, to make their views known to the IPSASB, and ensures that all views are considered in the standard-setting development process.

Governance

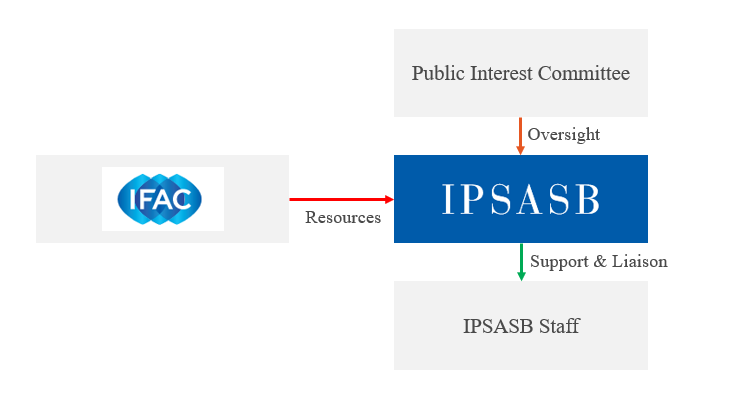

Following the report of the IPSASB Governance Review Group in 2015, the Public Interest Committee (PIC) was established. The PIC’s remit is to provide assurance that the IPSASB’s standard-setting activities are in the public interest by providing recommendations on:

- The terms of reference of the IPSASB;

- The arrangements for nomination and appointment of IPSAB members; and

- The procedures and processes for formulation of the IPSASB’s strategy and work plan; and development of IPSAS.

The PIC is currently comprised of individuals from the International Monetary Fund, International Organisation of Supreme Audit Institutions, Organisation for Economic Co-operation and Development, and the World Bank Group.

Key Contacts

-

Members

Members

-

Funding and Funding Opportunities

The IPSASB’s work, including the standards program, would not be possible without the support of our funding partners that are committed to strengthening the public sector. The IPSASB is funded entirely by voluntary, non-restrictive contributions (both financial and in-kind). We are grateful for the continued generosity and commitment of our current funding partners. In addition to those listed below, the IPSASB also receives support from others, such as hosts for meetings and outreach engagements throughout the year and receives in-kind support from its 17 volunteer members from around the world, its technical advisors and its official observers.

Funding Partners

ASIAN DEVELOPMENT BANK

CHARTERED PROFESSIONAL ACCOUNTANTS OF CANADA

GOVERNMENT OF CANADA

NEW ZEALAND EXTERNAL REPORTING BOARD

THE WORLD BANK

As implementation of the IPSASB Standards increases globally, the demands on the IPSASB’s resources grow. We are therefore committed to further diversifying our funding base to meet these growing demands. We encourage all users of the IPSASB Standards and those that are committed to strengthening public financial management globally through increasing adoption of accrual-based IPSAS and Sustainability Reporting Standards to become funding partners. Please email rosssmith@ipsasb.org for more information.

INTERNATIONAL FEDERATION OF ACCOUNTANTS (IFAC)

The IPSASB’s primary funder is IFAC. IFAC support contributes to the development, adoption and implementation of high-quality international standards.

The IPSASB and IFAC operate in principle at arm’s length in fulfilling their respective mandates:

- IFAC does not interfere with the independent decision-making process of the IPSASB;

- IFAC does not exert influence on the IPSASB chair, IPSASB members or staff in any way that affects the ability of such persons to act independently; and

- IFAC funding is provided based on the IPSASB’s annual budget request to support its operational plan, subject to IFAC financial envelope approved by IFAC Council. The IPSASB budget request is developed by IPSASB staff in consultation with IPSASB Chair.

IFAC provides adoption and implementation support and facilitates the work of the IPSASB, and the other independent standard-setting boards, through in-kind support in areas such as communications, finance, human resources, and intellectual property management.

IPSASB Relationship with IFAC

-

History

What would later become the IPSASB first originated in 1986 when IFAC, the global voice of the accountancy profession, established the Public Sector Committee (PSC) as a standing committee with a broad mandate to develop programs to improve public financial management and accountability. Over the next 10 years, the PSC issued studies on specialized accounting issues in the public sector. In 1996, the PSC changed its role to an international accounting standard setter for the public sector with the launch of its Standards Program. In 2004, the PSC was relaunched as the IPSASB with revised terms of reference to reflect the Board's mandate to focus on developing and issuing IPSASs.

-

Biennial Reports

-

Terms of Reference

OBJECTIVE

The International Public Sector Accounting Standards Board’s (IPSASB®) objective is to serve the public interest by developing high-quality accounting and sustainability standards and other material for use by public sector entities around the world in the preparation of general purpose financial reports (GPFR).

This is intended to enhance the quality and transparency of public sector financial and sustainability reporting by providing better information for public sector financial management, sustainability development, accountability and decision making. In pursuit of this objective, the IPSASB supports the convergence of international and national public sector accounting and sustainability standards and the alignment of accounting and statistical bases of financial reporting where appropriate; and also promotes the acceptance of its standards and other publications.

PRONOUNCEMENTS

In fulfilling the above objective, the IPSASB develops and issues, under its own authority, the following:

- International Public Sector Accounting StandardsTM (IPSAS®) as the authoritative accounting standards.

- IPSASB Sustainability Reporting StandardsTM (IPSASB SRSTM) as the authoritative sustainability standards.

- Other non-authoritative material such as the following:

- The Conceptual Framework establishes the concepts that are to be applied in developing IPSAS Accounting Standards and IPSASB SRS Standards.

- Recommended Practice GuidelinesTM (RPGTM) applicable to the preparation and presentation of GPFR to provide guidance that represents good practice that public sector entities are encouraged to follow.

- Studies to provide advice on financial and sustainability reporting issues in the public sector. They are based on study of the best practices and most effective methods for dealing with the issues being addressed.

- Other papers and research reports to provide information that contributes to the body of knowledge about public sector financial and sustainability reporting issues and developments. They are aimed at providing new information or fresh insights and generally result from research activities such as: literature searches, questionnaire surveys, interviews, experiments, case studies and analysis.The official text of the IPSAS Accounting Standards, IPSASB SRS Standards and other material is that published by the IPSASB in the English language.

The official text of the IPSAS Accounting Standards, IPSASB SRS Standards and other material is that published by the IPSASB in the English language.

MEMBERSHIP

The members of the IPSASB, including the Deputy Chair, but not the Chair, are appointed by the IFAC Board on the recommendation of the IFAC Nominating Committee , with consideration of advice from the Public Interest Committee (PIC). The IFAC Board provides the PIC with a written report and documentation supporting the application of the nomination due process.

The IPSASB has 18 members, including the Chair, of whom no less than three shall be public members. A public member is expected to reflect, and be seen to reflect, the wider public interest. Members may be nominated by governments, IFAC Member Bodies, the Forum of Firms, public agencies, international organizations, or the general public.

The selection process is based on the principle of “most suitable person for the job,” the primary criterion being the individual qualities and abilities of the nominee in relation to the position for which they are being nominated. However, the selection process also seeks a balance between the personal and professional qualifications of a nominee and representational needs, including gender balance, geographic representation, sector of the accountancy profession, sustainability expertise, knowledge of institutional arrangements encompassed by its constituency, size of the organization, and level of economic development.

IPSASB members may be accompanied at meetings by a technical advisor. A technical advisor, with the consent of the IPSASB member he or she advises, is entitled to participate in the discussions and deliberations at meetings and may participate in projects. Technical advisors are expected to possess the technical skills to participate, as appropriate, in IPSASB debates and attend IPSASB meetings regularly to maintain an understanding of current issues relevant to their role.

Observers, such as representatives of appropriate organizations that have a strong interest in financial reporting in the public sector, provide ongoing input to the work of the IPSASB and have an interest in endorsing and supporting IPSAS, may be appointed[1]. Observers are expected to attend IPSASB meetings regularly. They are entitled to participate in the discussions and deliberations at meetings, and may also participate in projects. Observers are expected to possess the technical skills to participate fully in IPSASB debates. The IPSASB will review the composition and role of observers on a periodic basis.

IPSASB members and technical advisors are required to sign an annual statement declaring they will not submit to undue influence, whether financial or otherwise, which might impair their ability to serve or act as a member or technical advisor with independence, integrity and in the public interest. Nominating organizations of members of the IPSASB and the employing organization of the Chair of the IPSASB (as applicable) are asked to sign similar independence declarations.

The Chair of the IPSASB Consultative Advisory Group (CAG) may attend IPSASB meetings, or appoint a representative of a CAG member organization to attend. The Chair of the IPSASB CAG, or appointed representative, is entitled to participate in the discussions and deliberations at IPSASB meetings.

Members of the PIC have the right to attend, or be represented at, all IPSASB meetings.

THE IPSASB CHAIR

A recommendation for the appointment of the IPSASB Chair is made by the IFAC Nominating Committee or an independent standard-setting board nominating committee/search committee. The recommendation is submitted to the PIC to review and then to the IFAC Board for its approval. To enhance independence, an independent standard-setting board nominating committee/search committee is the preferred option for making the recommendation for the IPSASB Chair. However, IFAC, with the consideration of the advice of the PIC, can also use the IFAC Nominating Committee for this purpose.

Where the IPSASB Chair is a remunerated position, IFAC holds a contract for service with the Chair as part of IFAC’s support of the IPSASB.

THE IPSASB DEPUTY CHAIR

The appointment as IPSASB Deputy Chair is considered a leadership position in support of the Chair and does not imply that the individual concerned is the Chair-elect.

In the event of a permanent vacancy, such as by reason of the incapacity, resignation, removal or death of the Chair, the IFAC Nominating Committee or any independent standard-setting board nominating committee/search committee, as applicable, has the authority to fill such vacancy in accordance with the IFAC Bylaws, with consideration of advice of the PIC. As a general rule, the Deputy Chair would be appointed to assume the duties of the Chair as acting Chair, having full power, authority and responsibility of the role of the Chair to manage the Board’s agenda and work program until the appointment of an interim or a new Chair.

TERMS OF OFFICE

Each term of office for an IPSASB member shall be for a period of not more than three years, with an intention for approximately one-third of the membership rotating each year. A member may serve consecutive terms, for up to an aggregate of six years.

The Chair is appointed for a term of up to three years and could be recommended for reappointment for additional terms not exceeding three years each until he/she has reached the maximum of nine consecutive years. In exceptional circumstances, to be specified by the IFAC Nominating Committee, the term of the Chair may be extended for up to three more years, for a total term as Chair not exceeding twelve years.

MEETING PROCEDURES

Each IPSASB meeting requires the presence, in person or by simultaneous telecommunications link, of at least twelve appointed members.

IPSASB meetings shall be chaired by the Chair, or in his/her absence, by the Deputy Chair. In the event of the absence of both, the members present shall select one of their number to take the chair for the duration of the meeting, or of the absence of the Chair and Deputy Chair.

Each member of the IPSASB, including the Chair, has one vote which can be exercised only by the appointed member. The affirmative vote of at least twelve of those present at a meeting in person or by simultaneous telecommunications link is required to approve or withdraw IPSAS Accounting Standards, IPSASB SRS Standards, RPG Guidelines, or the Conceptual Framework, and to approve Consultation Papers, strategy documents, and exposure drafts.

IPSASB meetings to discuss the development, and to approve the issuance or withdrawal of standards or other technical documents are open to the public. Matters of a general administrative nature or with privacy implications may be dealt with in closed sessions of the IPSASB; no decisions that would affect the content of the IPSAS Accounting Standards, IPSASB SRS Standards, and other pronouncements issued by the IPSASB are made in a closed session. Agenda papers for open sessions, including minutes of the meetings of the IPSASB, are published on the IPSASB’s website. The meetings and agenda papers are in English, which is the official working language of the IPSASB.

DUE PROCESS

The IPSASB is required to be transparent in its activities, and in developing IPSAS Accounting Standards and IPSASB SRS Standards to adhere to due process, which is set and agreed based on advice of the PIC. The IPSASB provides the PIC with documentation supporting the application of due process for all new or revised IPSAS Accounting Standards or IPSASB SRS Standards before their release. The PIC’s consideration of due process may require the IPSASB to take further steps to address concerns regarding the application of due process, if raised.

The IPSASB provides the PIC with documentation supporting the application of due process followed to develop the strategy and work plan and obtains the views of the PIC on whether due process has been followed effectively.

In setting its strategy and work plan, the IPSASB also obtains the PIC’s advice on the appropriateness of the items on the work plan, and on the completeness of the strategy and work plan from a public interest perspective. The IPSASB adjusts its final work plan to reflect the public interest views of the PIC or explains to the PIC how it has taken into account its advice. The IPSASB also discusses progress on its strategy and work plan with the PIC on a regular basis.

The IPSASB issues exposure drafts of all proposed IPSAS Accounting Standards, IPSASB SRS Standards, and RPG Guidelines for public comment. In some cases, the IPSASB may also issue a Consultation Paper prior to the development of an exposure draft. This provides an opportunity for those affected by IPSASB pronouncements to provide input and present their views before the pronouncements are finalized and approved. The IPSASB considers all comments received on Consultation Papers and exposure drafts in developing an IPSAS Accounting Standards, IPSASB SRS Standards, or RPG Guidelines.

The IPSASB cooperates with national standard setters in preparing and issuing IPSAS Accounting Standards, IPSASB SRS Standards, and RPG Guidelines to the extent possible, with a view to sharing resources, minimizing duplication of effort and reaching consensus and convergence in standards at an early stage in their development. It also promotes the endorsement of IPSAS Accounting Standards, IPSASB SRS Standards, and RPG Guidelines by national standard setters and other authoritative bodies and encourages consultation with users, including elected and appointed representatives, Treasuries, Ministries of Finance and similar authoritative bodies, and practitioners throughout the world to identify user needs for new standards and guidance.

In developing its pronouncements, the IPSASB seeks input from its Consultative Advisory Group and considers and makes use of pronouncements issued by:

- The International Accounting Standards Board (IASB®) and International Sustainability Standards Board (ISSBTM) to the extent they are applicable to the public sector;

- National standard setters, regulatory authorities and other authoritative bodies;

- International organizations responsible for the development of statistical bases of financial reporting;

- Professional accountancy organizations; and

- Other organizations interested in financial reporting in the public sector.

The IPSASB will ensure that its pronouncements are aligned with those of IASB and ISSB to the extent those pronouncements are applicable and appropriate to the public sector.

CONSULTATIVE GROUP

The objective of the IPSASB Consultative Advisory Group (CAG) is to provide input to and assist the IPSASB through consultation with the CAG member organizations and their representatives at the CAG meetings. The CAG provides advice on the IPSASB’s agenda and work program, including project priorities and timetables, technical advice on projects and advice on other matters of relevance to the activities of the IPSASB.

OTHER

The IPSASB annual report outlines its work program, activities and progress made in achieving its objectives during the year.

The IFAC Board will review the terms of reference of the IPSASB at least every five years, considering advice from the PIC. The PIC may also on an ad hoc basis provide advice on proposed changes to the terms of reference.

IFAC provides financial, operational and administrative support to the IPSASB and, if applicable, in consultation with the PIC. IFAC does not interfere with the independent decision-making process of the IPSASB as the IPSASB carries out its public interest function under these terms of reference.

[1] Article 25.1 (e) of the IFAC Bylaws states that the IFAC Board shall approve the appointment of any observers of any independent SSB. However, at its February 2025 meeting, the Board supported allowing the IPSASB to make appointments of observers and agreed to delegate its authority to the IPSASB to do so.