The Board approved the Final Pronouncement, Definition of Material (Amendments to IPSAS 1, IPSAS 3, and the Conceptual Framework), enhancing the clarity and consistent application of materiality in IPSAS Standards. The amendments to IPSAS Standards are effective January 1, 2027, and amendments to the Conceptual Framework are effective upon publication of the pronouncement.

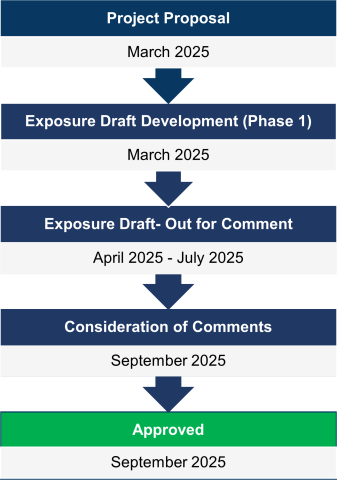

Project Timeline

The project timeline is depicted below. Please note that these are current targeted milestones/phases and may change as the work in this area progresses.

Image

Project Overview

Objective

The objective of this project is to:

- Clarify that an entity is required to consider the information needs of primary users instead of other users of GPFRs; and

- Align the definition of material in IPSAS 1, Presentation of Financial Statements, with Chapter 3 of the Conceptual Framework on Qualitative Characteristics.

This will ensure that general-purpose financial statements (GPFS) provide relevant information to users for accountability and decision-making purposes.

Why the IPSASB Undertook this Project

The IPSASB proposed adding the Making Materiality Judgements project because feedback received highlighted that some entities have difficulties making materiality judgments and tend to use disclosure requirements in IPSAS® Accounting Standards as a checklist instead of applying judgement on what information is material and should be included in the general-purpose financial statements (GPFS).

Task Force Members

No Task Force was appointed for this project

Contact

Published Documents and Support

Documents in this section include:

- Major documents published by the IPSASB during the lifecycle of the project including: Consultation Papers, Exposure Drafts, issued IPSAS, amendments to IPSAS, and other similar due process documents;

- Supporting material related to each published document including: snapshots, webinars, and other material; and

- The project-relevant IPSASB agenda papers.

Content

Content

Content

Content

Content