Definition of Material (Amendments to IPSAS 1, IPSAS 3, and the Conceptual Framework)

IPSASB

| Handbooks, Standards, and Pronouncements

English

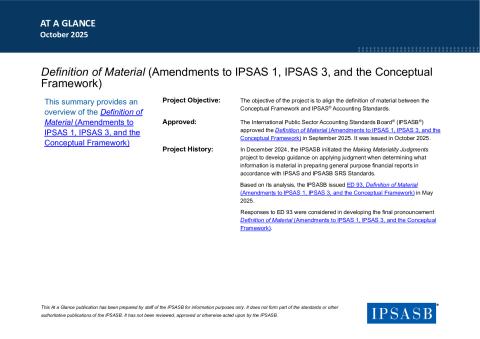

This pronouncement conforms the definition of the term material between the Conceptual Framework and within IPSASB’s authoritative guidance and lays the foundation for planned guidance on materiality judgments in financial reporting. It clarifies that general-purpose financial reports are prepared to meet the information needs of primary users for accountability and decision-making purposes.

The effective date of the amendments to IPSAS Standards is January 1, 2027, with the Conceptual Framework becoming effective upon publication of this pronouncement.

Copyright © 2026 The International Federation of Accountants (IFAC). All rights reserved.