IPSAS Exposure Draft (ED) 93, Definition of Material (Amendments to IPSAS 1, IPSAS 3, and the Conceptual Framework)

IPSASB

| Exposure Drafts and Consultation Papers

English

Comments due by:

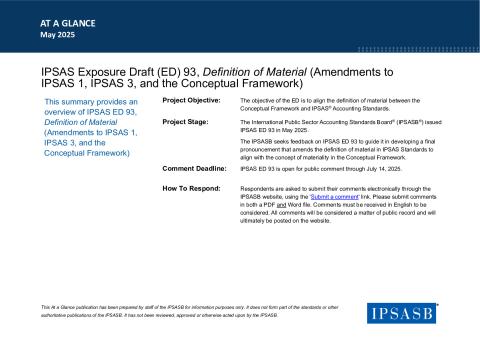

The objective of IPSAS ED 93 is to align the definition of material between the Conceptual Framework and IPSAS Accounting Standards. IPSAS ED 93 proposes to clarify that an entity is required to consider the information needs of primary users instead of other users of general purpose financial reports when applying the concept of materiality. To achieve this, we propose to add ‘primary’ before ‘users’ to the concept of materiality, described in paragraph 3.32 in the Conceptual Framework.

IPSAS ED 93 is open for public comment through July 14, 2025. Comments must be submitted in English.

Copyright © 2026 The International Federation of Accountants (IFAC). All rights reserved.

Submitted Comment Letters

-

The Institute of Chartered Accountants of Nigeria (ICAN) (184.83 KB)(Nigeria)

-

North Atlantic Treaty Organization (NATO) (153.26 KB)(- International)

-

Mo Chartered Accountants (Zimbabwe) (125.67 KB)(Zimbabwe)

-

Ricky A. Perry, Jr. (137.03 KB)(United States of America)

-

Conseil de Normalisation des Comptes Publics (CNOCP) (1.85 MB)(France)

-

International Labour Organisation (ILO) (242.23 KB)(- International)

-

External Reporting Board (XRB) (365.41 KB)(New Zealand)

-

Association of Chartered Certified Accountants (ACCA) (79.84 KB)(- International)

-

Accounting Standards Board (ASB) (226.02 KB)(South Africa)

-

Conselho Federal de Contabilidade (CFC) (743.71 KB)(Brazil)

-

Chartered Accountants Australia and New Zealand (CA ANZ) and CPA Australia (182.5 KB)(Australia)

-

Accountancy Europe (83.67 KB)(- International)

-

Colegio de Contadores Publicos de Pichincha y del Ecuador (199.02 KB)(Ecuador)

-

Forvis Mazars (219.94 KB)(Belgium)

-

Institute of Certified Public Accountants of Kenya (ICPAK) (292.09 KB)(Kenya)

-

Institute of Chartered Accountants of India (156.71 KB)(India)

-

Kalar Consulting Ltd (476.93 KB)(United Kingdom)

-

Malaysian Institute of Accountants (MIA) (211.12 KB)(Malaysia)

-

Ministry of Finance (125.41 KB)(Saudi Arabia)

-

Public Sector Accounting Standards Board (PSASB) (356.5 KB)(Kenya)

-

South African Institute of Chartered Accountants (SAICA) (561.69 KB)(South Africa)

-

Swiss Public Sector Financial Reporting Advisory Committee (SRS-CSPCP) (180.3 KB)(Switzerland)

-

Public Accountants and Auditors Board (PAAB) (394.77 KB)(Zimbabwe)

-

Forum of Governmental Accounting of Latin America (FOCAL) (1.08 MB)(Chile)

-

Forum of Governmental Accounting of Latin America (FOCAL) (1.08 MB)(Colombia)

-

Forum of Governmental Accounting of Latin America (FOCAL) (1.08 MB)(El Salvador)

-

Forum of Governmental Accounting of Latin America (FOCAL) (1.08 MB)(Guatemala)

-

Forum of Governmental Accounting of Latin America (FOCAL) (1.08 MB)(Dominican Republic)

-

Forum of Governmental Accounting of Latin America (FOCAL) (1.08 MB)(República de Venezuela)

-

Forum of Governmental Accounting of Latin America (FOCAL) (975.17 KB)(Peru)