IESBA’s snapshots provide short, non-technical overviews of IESBA projects or workstreams. They explain the purpose, direction, and current focus in clear and accessible terms, alongside more detailed technical materials.

This Snapshot focuses on IESBA’s Post-Implementation Reviews (PIRs).

Q1. What is a Post-Implementation Review (PIR)?

A PIR is a process that aims to assess whether a given IESBA standard is achieving its intended objectives by identifying benefits achieved and implementation challenges, and to inform any actions the IESBA may need to take in response.

For further details of how and when a PIR might be initiated, please refer to paragraphs A42 to A44 of the IESBA’s Integrated Due Process and Public Interest Framework (PIF) Operating Procedures.

Q2. Why is the IESBA undertaking these two PIRs?

As part of its 2024–2027 Strategy and Work Plan, the IESBA committed to conducting PIRs to evaluate whether certain key standards are operating as intended in practice. Standards to be covered by these PIRs included:

- The Responding to Non-Compliance with Laws and Regulations (NOCLAR) provisions released in July 2016 and effective July 2017.

- The Restructured Code released in April 2018 and effective June 2019.

The PIRs also respond to calls from stakeholders to evaluate the real-world effectiveness of the implementation of major ethics standards.

Q3. What is the NOCLAR® Standard? Why was it developed?

The NOCLAR standard establishes a first-of-its-kind framework to guide professional accountants in how best to respond to actual or suspected NOCLAR committed by a client or employer, those working in a management or governance role within the client or employer, or others working for or under its direction, in the public interest.

It provides a clear, globally consistent path for professional accountants to respond to instances of NOCLAR or suspected NOCLAR, taking into account their responsibility to act in the public interest.

Q4. What were the main changes and objectives of the Restructured Code?

The Restructured Code enhanced the clarity, usability, and enforceability of the IESBA Code through a more intuitive structure, clearer drafting conventions, and the use of plain English.

Its objectives were to improve understanding and consistent application of the fundamental principles of ethics, facilitate global adoption and translation, and strengthen confidence in the Code as the international benchmark for ethical behavior in the accountancy profession.

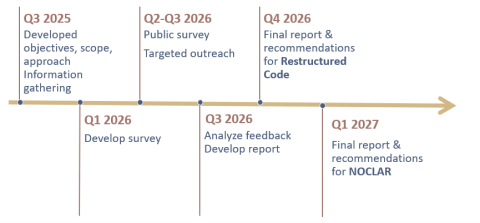

Q5. How will the PIRs be undertaken?

Planning commenced in Q3 2025, including coordination with the International Auditing and Assurance Standards Board (IAASB) to align objectives and approaches for PIRs. Information will be gathered through:

- Public surveys (released on April 1, 2026, for 90–120 days) designed for key stakeholder groups, including regulators, standard setters, professional accountancy organizations, firms, professional accountants, preparers, those charged with governance, investors, and other users.

- Targeted outreach to gain a deeper understanding of real-world impacts.

- Desktop research to supplement survey and outreach findings.

Q6. How will the surveys be conducted and what feedback will be asked?

The surveys will be customizable by stakeholder type and structured to allow respondents to comment on one or both PIRs.

The surveys will gather insights on:

- Adoption – whether and how the provisions have been adopted, including any modifications and reasons for such modifications;

- Implementation – challenges faced and lessons learned;

- Enforcement – enforcement responsibilities at the local level; and

- Impact – benefits and outcomes achieved and factors influencing success.

Q7. What are the expected outputs and timeline for the project?

The key expected outputs of the project include:

- April 1, 2026 – Launch of public surveys (open for 90–120 days).

- December 2026 – Final Restructured Code PIR report and recommendations to the IESBA.

- March 2027 – Final NOCLAR PIR report and recommendations to the IESBA.

Q8. How will the findings of the PIRs be used?

The results will inform the IESBA’s assessment of whether any further actions are necessary regarding these standards.

Based on the findings, the IESBA may conclude that no further action is required or take one or more of the following actions:

- Undertake further information-gathering;

- Initiate standard-setting; or

- Develop non-authoritative materials or other initiatives.

Q9. Where can stakeholders find more information?

To learn more about these projects, explore their project pages:

Q10. Who can stakeholders contact?

For any queries, please reach out to: Kam Leung, IESBA Director, at kamleung@ethicsboard.org.

About IESBA

The International Ethics Standards Board for Accountants (IESBA) is an independent global standard-setting board. The IESBA’s mission is to serve the public interest by setting high-quality, international ethics (including independence) standards as a cornerstone to ethical behavior in business and organizations, and to public trust in financial and non-financial information that is fundamental to the proper functioning and sustainability of organizations, financial markets and economies worldwide.

Along with the International Auditing and Assurance Standards Board (IAASB), the IESBA is part of the International Foundation for Ethics and Audit (IFEA). The Public Interest Oversight Board (PIOB) oversees IESBA and IAASB activities and the public interest responsiveness of the standards.