Exposure Draft 71, Revenue without Performance Obligations

IPSASB

| Exposure Drafts and Consultation Papers

English

Comments due by:

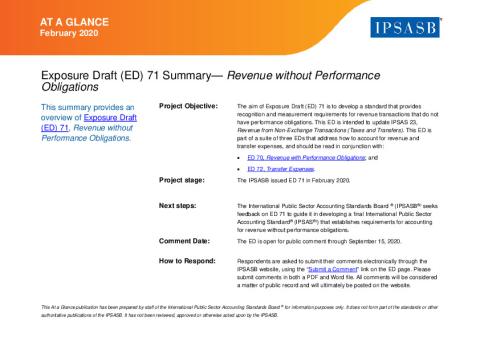

The aim of Exposure Draft (ED) 71 is to develop a standard that provides recognition and measurement requirements for revenue transactions that do not have performance obligations. This ED is intended to update IPSAS 23, Revenue from Non-Exchange Transactions (Taxes and Transfers). This ED is part of a suite of three EDs that address how to account for revenue and transfer expenses, and should be read in conjunction with:

Please submit your comments by November 1, 2020.

Copyright © 2026 The International Federation of Accountants (IFAC). All rights reserved.

Submitted Comment Letters

-

Comissão de Normalização Contabilística (128.1 KB)(Portugal)

-

Tiago Melo (351.31 KB)(Portugal)

-

Auckland Council (409.08 KB)(New Zealand)

-

Vincenzo Cordaro (1.97 MB)(Italy)

-

Swiss Public Sector Financial Reporting Advisory Committee (218.7 KB)(Switzerland)

-

CNoCP (125.75 KB)(France)

-

Accountancy Europe (172.44 KB)()

-

Treasury Board of Canada Secretariat (207.62 KB)(Canada)

-

Office of the Auditor General of Alberta (560.01 KB)()

-

Public Sector Accounting Standards Board (2.31 MB)(Kenya)

-

Task force IRSPM A&A SIG, CIGAR Network, EGPA PSG XII (168.22 KB)()

-

Accrual Accounting Center (415.76 KB)()

-

Institute of Chartered Accountants Ghana (1.33 MB)(Ghana)

-

Pan African Federation of Accountants (PAFA) (224.53 KB)()

-

CPA Australia and Chartered Accountants Australia and New Zealand (147.65 KB)()

-

Australia Accounting Standards Board (AASB) (422.12 KB)(Australia)

-

NSW Treasury (315.28 KB)(Australia)

-

The Japanese Institute of Certified Public Accountants (248.85 KB)(Japan)

-

Accounting Standard Board (South Africa) (374.9 KB)(South Africa)

-

Korea Institute of Public Finance (GAFSC) (392.19 KB)(Korea)

-

CIPFA (258.78 KB)(United Kingdom)

-

PSAB Staff (218.34 KB)(Canada)

-

ACCA (234.96 KB)()

-

KPMG LLP (88.57 KB)(Canada)

-

PwC (157.48 KB)()

-

UNDP (908.83 KB)()

-

a. Foro de Contadurias Gubernamentales de America Latina (FOCAL) - Brazil (735.79 KB)()

-

b. Foro de Contadurias Gubernamentales de America Latina (FOCAL) - Chile (735.82 KB)()

-

c. Foro de Contadurias Gubernamentales de America Latina (FOCAL) - Colombia (735.78 KB)()

-

d. Foro de Contadurias Gubernamentales de America Latina (FOCAL) - Costa Rica (735.8 KB)()

-

e. Foro de Contadurias Gubernamentales de America Latina (FOCAL) - Ecuador (735.78 KB)()

-

f. Foro de Contadurias Gubernamentales de America Latina (FOCAL) - El Salvador (735.77 KB)()

-

g. Foro de Contadurias Gubernamentales de America Latina (FOCAL) - Guatemala (735.8 KB)()

-

h. Foro de Contadurias Gubernamentales de America Latina (FOCAL) - Honduras (735.8 KB)()

-

i. Foro de Contadurias Gubernamentales de America Latina (FOCAL) - Mexico (735.81 KB)()

-

j. Foro de Contadurias Gubernamentales de America Latina (FOCAL) - Paraguay (735.79 KB)()

-

k. Foro de Contadurias Gubernamentales de America Latina (FOCAL) - Peru (735.79 KB)()

-

Donald Love (75.47 KB)(United States of America)

-

ICAEW (221.16 KB)()

-

Institute of Chartered Accountants of Nigeria (311.2 KB)(Nigeria)

-

Botswana Institute of Chartered Accountants (195.41 KB)(Botswana)

-

CONSELHO FEDERAL DE CONTABILIDADE (330.51 KB)(Brazil)

-

Office of the Auditor General of Canada (866.34 KB)(Canada)

-

EY (171.97 KB)()

-

NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS - TANZANIA (464.24 KB)(Tanzania, United Republic of)

-

Office of the Comptrolle General, British Columbia (275 KB)(Canada)

-

Governmental Accounting Standards Board (804.04 KB)(United States of America)

-

European Commission (472.15 KB)()

-

Financial Reporting Council of Nigeria (301.1 KB)(Nigeria)

-

New Zealand Accounting Standards Board (643.52 KB)(New Zealand)