Exposure Draft 70, Revenue with Performance Obligations

IPSASB

| Exposure Drafts and Consultation Papers

English

Comments due by:

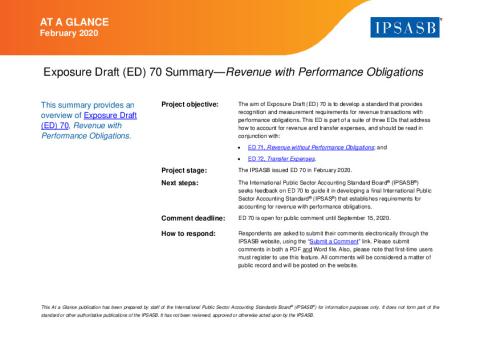

The aim of Exposure Draft (ED) 70 is to develop a standard that provides recognition and measurement requirements for revenue transactions with performance obligations. This ED is part of a suite of three EDs that address how to account for revenue and transfer expenses, and should be read in conjunction with:

Please submit your comments by November 1, 2020.

Copyright © 2026 The International Federation of Accountants (IFAC). All rights reserved.

Submitted Comment Letters

-

Michel Maher, Avocat, CPA, LLM, LLD (96.47 KB)(Canada)

-

Comissão de Normalização Contabilística (129.26 KB)(Portugal)

-

Tiago Melo (351.19 KB)(Portugal)

-

Vincenzo Cordaro (1.97 MB)(Italy)

-

Swiss Public Sector Financial Reporting Advisory Committee (219.58 KB)(Switzerland)

-

ITER Organization (603.76 KB)()

-

Office of the Auditor General of Ontario (186.59 KB)()

-

CNoCP (117.93 KB)(France)

-

Accountancy Europe (172.44 KB)()

-

Treasury Board of Canada Secretariat (165.5 KB)(Canada)

-

New Zealand Accounting Standards Board (643.52 KB)()

-

Public Sector Accounting Standards Board (2.04 MB)(Kenya)

-

Task force IRSPM A&A SIG, CIGAR Network, EGPA PSG XII (138.99 KB)()

-

Australian Accounting Standards Board (422.12 KB)()

-

Pan African Federation of Accountants (PAFA) (224.03 KB)()

-

Accrual Accounting Center (392.11 KB)()

-

Institute of Chartered Accountants Ghana (1.02 MB)(Ghana)

-

Public Sector Accounting Board Staff (192.71 KB)(Canada)

-

CPA Australia and Chartered Accountants Australia and New Zealand (138.16 KB)()

-

The Malaysian Institute of Certified Public Accountants (MICPA) (126.93 KB)(Malaysia)

-

NSW Treasury (315.28 KB)(Australia)

-

The Japanese Institute of Certified Public Accountants (283.34 KB)(Japan)

-

Institute of Certified Public Accountants of Rwanda (ICPAR) (889.62 KB)(Rwanda)

-

South African Accounting Standards Board (308.29 KB)(South Africa)

-

Korea Institute of Public Finance (GAFSC) (294.76 KB)(Korea)

-

CIPFA (258.78 KB)(United Kingdom)

-

United Nations Office for Project Services (124.43 KB)()

-

ACCA (234.96 KB)()

-

KPMG LLP (88.57 KB)(Canada)

-

PwC (151.24 KB)()

-

UNDP (908.83 KB)()

-

Secretaria de hacienda y credito publico, especificamente la unidad de contabilidad gubernamental – Mexico (889.26 KB)()

-

Institute of Chartered Accountants of Nigeria (307.17 KB)(Nigeria)

-

ICAEW (222.39 KB)()

-

Office of the Auditor-General (290.62 KB)(New Zealand)

-

Botswana Institute of Chartered Accountants (180.89 KB)(Botswana)

-

CONSELHO FEDERAL DE CONTABILIDADE (312.81 KB)(Brazil)

-

NATIONAL BOARD OF ACCOUNTANTS AND AUDITORS - TANZANIA (457.95 KB)(Tanzania, United Republic of)

-

EY (154.64 KB)()

-

Governmental Accounting Standards Board (804.04 KB)(United States of America)

-

Office of the Comptrolle General, British Columbia (240.21 KB)(Canada)

-

Financial Reporting Council of Nigeria (195.48 KB)(Nigeria)

-

a. Foro de Contadurias Gubernamentales de America Latina (FOCAL) - Mexico (777.88 KB)()

-

b. Foro de Contadurias Gubernamentales de America Latina (FOCAL) - Paraguay (777.89 KB)()

-

c. Foro de Contadurias Gubernamentales de America Latina (FOCAL) - Peru (777.89 KB)()

-

d. Foro de Contadurias Gubernamentales de America Latina (FOCAL) - Honduras (777.89 KB)()

-

e. Foro de Contadurias Gubernamentales de America Latina (FOCAL) - Guatemala (777.91 KB)()

-

f. Foro de Contadurias Gubernamentales de America Latina (FOCAL) - El Salvador (777.87 KB)()

-

g. Foro de Contadurias Gubernamentales de America Latina (FOCAL) - Ecuador (777.88 KB)()

-

h. Foro de Contadurias Gubernamentales de America Latina (FOCAL) - Costa Rica (777.91 KB)()