Exposure Draft 64, Leases

IPSASB

| Exposure Drafts and Consultation Papers

English

Comments due by:

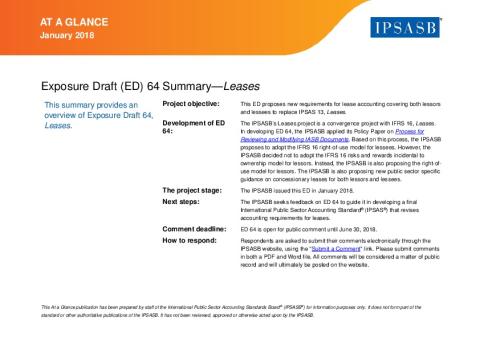

The International Public Sector Accounting Standards Board (IPSASB) has issued Exposure Draft 64, Leases.

The Exposure Draft proposes a single right-of-use model for lease accounting that will replace the risks and rewards incidental to ownership model in IPSAS 13, Leases.

For lessees, ED 64 proposes accounting requirements that are converged with IFRS 16, Leases issued by the International Accounting Standards Board. For lessors, ED 64 proposes a right-of-use model specifically designed for public sector financial reporting.

ED 64 also proposes new public sector specific accounting requirements for leases at below market terms (also known as "concessionary leases") for both lessors and lessees.

Copyright © 2026 The International Federation of Accountants (IFAC). All rights reserved.

Submitted Comment Letters

-

Alvaro Fonseca Vivas (33.04 KB)()

-

The Institute of Certified Public Accountants in Ireland (419.48 KB)(Ireland)

-

The Institute Of Chartered Accountants (Ghana) (1.82 MB)(Ghana)

-

Auckland Council (5.04 MB)()

-

International Consortium on Government Financial Management (ICGFM) (133.91 KB)()

-

CNOCP (167.52 KB)()

-

Swiss Public Sector Financial Reporting Advisory Comittee (86.03 KB)(Switzerland)

-

Task force IRSPM A&A SIG, CIGAR Network, EGPA PSG XII (790.28 KB)()

-

Ichabod's Industries Ltd (566 KB)(United Kingdom)

-

CPA Australia (246.48 KB)()

-

The Japanese Institute of Certified Public Accountants (256.65 KB)(Japan)

-

Office of the Auditor-General, New Zealand (197.84 KB)(New Zealand)

-

Public Sector Accounting Standards Board Kenya (262.95 KB)(Kenya)

-

Pan African Federation of Accountants (262.11 KB)()

-

Treasury Board Secretariat Canada (118.79 KB)(Canada)

-

ACCA and CA ANZ (128.52 KB)()

-

The Treasury (2.22 MB)(New Zealand)

-

Wellington City Council (670.61 KB)()

-

Korea Institute of Public Finance (103.88 KB)(Korea)

-

Institut der Wirtschaftspruefer in Deutschland e.V. (IDW) (379.21 KB)(Germany)

-

Association of National Accountants of Nigeria - ANAN (207.05 KB)(Nigeria)

-

CIPFA (205.95 KB)(United Kingdom)

-

The Institute of Chartered Accountants of India (305.76 KB)(India)

-

PwC (467.37 KB)()

-

National Board Of Accountants And Auditors (342.55 KB)(Tanzania, United Republic of)

-

Accounting Standards Board (223.7 KB)(South Africa)

-

New Zealand Accounting Standards Board (910.67 KB)(New Zealand)

-

ICAEW (314.4 KB)(United Kingdom)

-

Australasian Council of Auditors-General (ACAG) (698.34 KB)()

-

Malaysian Institute of Accountants (817.03 KB)()

-

David Hardidge (518.12 KB)()

-

Ernst and Young GmbH (1.39 MB)()

-

European Commission (271.34 KB)()

-

Heads of Treasuries Accounting and Reporting Advisory Committee (HoTARAC) (417.24 KB)(Australia)

-

Kalar Consulting Ltd (112.5 KB)(United Kingdom)

-

Government of the Province of British Columbia (174.55 KB)(Canada)

-

Public Sector Accounting Board (218.69 KB)(Canada)

-

Conselho Federal de Contabilidade (CFC) (134.69 KB)(Brazil)

-

DGFiP (344.27 KB)(France)