Image

Advancing Public Sector Sustainability Reporting

Climate change affects everyone, transcending borders and economic boundaries. Rapid progress on climate change requires public sector action, and effective action requires the quality information only sustainability reporting standards specific to the sector’s needs can provide. Reporting on climate change is one of the most important issues in sustainability reporting today.

Public sector-specific sustainability reporting standards will encourage transparency, allowing governments to be held accountable for the long-term impacts of their interventions, enabling better-informed decision-making and access to critical financing streams including access to capital market inflows.

-

About the IPSASB Sustainability Reporting Standards

IPSASB standards are designed for public sector entities that meet the following three criteria:

- Are responsible for the delivery of services (encompassing goods, services and policy advice, including to other public sector entities) to benefit the public and/or to redistribute income and wealth;

- Mainly finance their activities, directly or indirectly, by means of taxes and/or transfers from other levels of government, social contributions, debt or fees; and

- Do not have the primary objective to make profits.

This includes a wide range of public sector entities, such as:

- National, regional, state/provincial and local governments;

- Government ministries, departments, programs, boards, commissions, agencies;

- Public sector social security funds, trusts and statutory authorities; and

- International governmental organizations.

In January 2026, the IPSASB published its inaugural IPSAS SRS Standard, the IPSASB SRS 1, Climate-related Disclosures.

The other sustainability reporting standard setting topics that IPSASB has identified for further research and scoping work are:

- General Requirements for Disclosure of Sustainability-related Financial Information; and

- Natural Resources – Non-Financial Disclosures (to be considered following the development of the financial reporting guidance proposed in its Exposure Draft 92, Natural Resources).

-

Other IPSASB Guidance

The IPSASB has strong foundations for reporting on programs addressing both climate change and the United Nations Sustainable Development Goals (SDGs) in its Recommended Practice Guideline (RPG) 3 on ‘Reporting Service Performance Information’. This can be applied now, together with RPG 1 ‘Reporting on the Long-Term Sustainability of an Entity’s Finances’ which can be used to bring together the financial impacts of non-financial metrics and risks being managed.

To support immediate application to sustainability reporting, the IPSASB issued Reporting Sustainability Program Information—Amendments to RPGs 1 and 3: Additional Non-Authoritative Guidance and Q&A: Climate Change: Relevant IPSASB Guidance which can be immediately applied by governments and public sector entities to report on sustainability program information. The additional guidance is intended to support the implementation of the key areas highlighted in the OECD paper Green Budgeting: A Way Forward.

-

History and Development of the IPSASB Sustainability Reporting Standards

The World Bank’s January 31, 2022 report, 'Sovereign Climate and Nature Reporting,' provided welcome further impetus to the critical issue of advancing sustainability reporting in the public sector. The report statistics that sovereign bonds make up almost 40% of the US$100 trillion global bond market is particularly striking. Together with the fact that national public sector expenditure is often the same percentage or more of GDP, this underlines both the urgency and importance of filling the current guidance gap.

In December 2022, the IPSASB decided to commence the scoping of three potential public sector specific sustainability reporting projects pending securing the resources needed to begin guidance development. This decision builds on IPSASB’s 25 years of public sector standard setting experience as well as the strong global stakeholder support for the proposals in its Consultation Paper, Advancing Public Sector Sustainability Reporting.

The Board’s prioritized research topics are:

- General Requirements for Disclosure of Sustainability-related Financial Information,

- Climate-Related Disclosures, and

- Natural Resources – Non-Financial Disclosures (to follow the development of financial reporting guidance proposed in its Natural Resources financial reporting project).

Following the scoping and research phase, the IPSASB decided to move forward with the development of a public sector specific Climate-Related Disclosures standard at its June 2023 meeting. The IPSASB SRS ED 1, Climate-related Disclosures, was exposed for public consultation in October 2024, and the IPSASB SRS 1, Climate-related Disclosures, was approved and published in January 2026, with support from the World Bank.

To support the development of sustainability reporting standards, the IPSASB established sustainability consultative groups, in addition to its existing financial reporting structures and due process, including the Consultative Advisory Group, to provide sustainability expertise advice to the Board.

-

IPSASB Sustainability Consultative Groups

The IPSASB Sustainability Reference Group (SRG) is an important part of the IPSASB’s sustainability standard setting work. The objective of the SRG is to provide an advisory forum where members with sustainability expertise can provide their input and advice on:

- The development of sustainability-related reporting standards for the public sector; and

- Relevant emerging sustainability reporting trends and issues.

The SRG will deliver on this objective by providing strategic advice on:

- The IPSASB’s overall sustainability strategy and work program;

- Individual projects, including views on key technical issues or matters that may impede the adoption or effective implementation of IPSASB sustainability reporting standards; and

- Other matters of relevance to the sustainability reporting standard-setting activities of the IPSASB.

Members of the SRG include:

- Alessandra Alfieri, United Nations Committee of Experts on Environmental-Economic Accounting

- Felipe Bardella, International Monetary Fund

- Andrew Blazey, Organisation for Economic Co-operation and Development

- Dmitri Gourfinkel, World Bank

- Alex Hill, CDP

- Anne-Claire Howard, United Nations Office for Project Services

- Patrick Kabuya, World Bank

- Marcos Mancini, United Nations Development Programme

- Emily McKenzie, Taskforce for Nature-related Financial Disclosures

- Paul Munter, Independent Standards Board Member, Greenhouse Gas Protocol

- Enrique Rebolledo, Asian Development Bank

- Bernard Schatz, Forum of Firms

- Bonnie Ann Sirois, World Bank

- Heather Taylor, A4S Canadian Circle of Practice

- Karma Tenzin, INTOSAI Development Initiative

- Sebastian Welisiejko, The Global Steering Group for Impact Investment

The Climate-related Topic Working Group (CTWG) is an important part of the development of the IPSASB SRS 1, Climate-related Disclosures. The objective of the CTWG is to provide climate-related expertise and advice to support delivery of the project. Members of the CTWG include international standard setters, from ISSB and GRI, and national standard setters advanced in the development of sustainability reporting standards, from Canada, the UK and New Zealand.

The IPSASB Sustainability Implementation Forum (SIF) is an open forum for public sector entities from around the world, across different levels of government, that are potential future users of the final IPSASB SRS Climate-related disclosures. Stakeholder engagement and feedback is of utmost importance in the development of sustainability reporting standards to ensure the principles proposed in draft standards can be implemented. The objective of the SIF is to gather feedback on the draft SRS based on real-life examples and practice and test whether the proposals in the draft SRS are implementable in order to inform the development of the SRS and implementation guidance and illustrative examples.

-

Resource Inventory

The following is a selection of existing supporting resources published by the IFRS Foundation, which may be relevant to support implementation of the IPSASB SRS 1, Climate-related Disclosures:

- IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information

- IFRS S2, Climate-related Disclosures

- Introduction to the ISSB Standards

- Making the Transition from TCFD to ISSB

- Voluntarily Applying ISSB Standards—A Guide for Preparers

- Educational material: Disclosing information about anticipated financial effects applying ISSB Standards

- Educational material: Greenhouse Gas Emissions Disclosure requirements applying IFRS S2 Climaterelated Disclosures

- Educational material: Sustainability-related risks and opportunities and the disclosure of material information

- Guidance document: Disclosing information about an entity’s climate-related transition, including information about transition plans, in accordance with IFRS S2

-

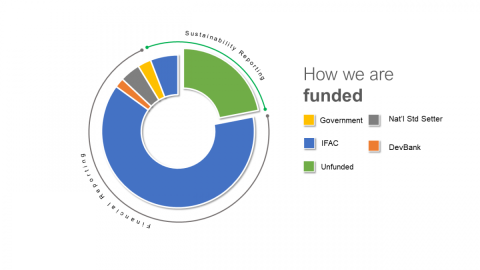

Funding Opportunities

The feedback received from stakeholders around the world is clear: the public sector needs its own specific sustainability reporting framework and the IPSASB should lead its development. But in addition to its existing expertise, IPSASB needs additional support, both financial and otherwise, from the global community in order to scale up its efforts and to move at pace to equip the public sector with the tools necessary to report on climate change and other sustainability issues.

The additional resources needed to take forward the development of public sector specific sustainability reporting standards need to be sufficient to enable the IPSASB to build a small, highly qualified, dedicated technical staff team to lead sustainability reporting standards development, as well as to support stakeholder engagement and the operations of the new Sustainability Reference Group.

The IPSASB is committed to the principle of diversified funding over time and envisions that new sources of funding will be earmarked for deployment for the specific purpose of advancing its sustainability work, rather than its financial reporting guidance program. Such additional sustainability reporting funding arrangements will be required to preserve and not interfere with the independent decision making of the IPSASB in its work.

Image

To contribute financial or other support to the IPSASB for the development of global public sector specific sustainability reporting standards, please email Ross Smith, IPSASB Program and Technical Director (rosssmith@ipsasb.org).