The IPSASB decided to move forward with the development of a public sector specific Climate-Related Disclosures standard and approved a project brief related to this major initiative. The IPSASB hopes to be able to initiate other sustainability-related projects in the coming months, subject to funding and resource availability. See the recent announcement for further information on how to get involved and support this critical initiative.

The IPSASB approved the updated Chapter 3, Qualitative Characteristics, which clarifies the role of prudence in public sector financial reporting and updates the guidance on materiality to better serve the users of financial information. The updated chapter is expected to be published in July 2023, and the project to revise the IPSASB’s Conceptual Framework is now complete.

Natural Resources

The IPSASB revised the project timelines to develop by March 2024 two EDs:

One to propose IPSAS guidance on natural resources; and

Another to propose an aligned IPSAS with IFRS 6, Exploration for and Evaluation of Mineral Resources.

The IPSASB intends to refine the definition and guidance on the accounting for natural resources to reflect the recognition challenges raised by constituents in comment letters to the 2022 Consultation Paper, Natural Resources.

Other Lease–Type Arrangements

The IPSASB undertook a first review of the responses to ED 84, Concessionary Leases and Right-of-Use Assets In-kind. The IPSASB agreed that the ED 84 proposals received strong support on balance, and that it should undertake a detailed review of the issues highlighted in the comments letters starting at the September 2023 meeting.

Measurement–Application Phase

The IPSASB agreed current operational value is not an applicable measurement basis for IPSAS 16, Investment Property; IPSAS 26, Impairment of Cash-Generating Assets; IPSAS 27, Agriculture; IPSAS 36, Investments in Associates and Joint Ventures; IPSAS 37, Joint Arrangements; and IPSAS 41, Financial Instruments. The IPSASB also decided the scope of its IPSAS 21, Impairment of Non-Cash-Generating Assets update should focus on the definition and components of ‘recoverable service amount’.

Retirement Benefit Plans

The IPSASB decided to update the disclosure requirements in [draft] IPSAS 49, Retirement Benefit Plansand clarify the objective and scope, by highlighting the requirements are only applicable to retirement benefit plans in the public sector. The IPSASB agreed this clarification would address concerns identified by respondents related to definitions and consolidation. The IPSASB plans to approve this new IPSAS at its September 2023 meeting.

Presentation of Financial Statements

The IPSASB decided the scope of the project is to replace IPSAS 1, Presentation of Financial Statements with a new IPSAS. The IPSASB further decided that because of the complexity of the topic, the use of a consultation paper is warranted to obtain stakeholder input to support the development of an ED. The IPSASB will further consider a draft project brief at the September 2023 meeting.

Differential Reporting

The IPSASB reflected on the findings and constituent input from the research and scoping activities, and how to best address the public needs that gave rise to a call for an international differential reporting model. The IPSASB agreed the development of other forms of guidance, rather than a standard-setting solution, may be more feasible and better address the public interest needs. The IPSASB will consider the types of guidance and the future approach for this project at its September 2023 meeting.

First-Time Adoption of Accrual Basis IPSASs

The IPSASB discussed feedback from jurisdictions with experience applying IPSAS 33. The IPSASB agreed steps should be taken to better enable the use of IPSAS 33 in practice. The IPSASB decided to consider alternatives on how it could improve IPSAS 33 at its September 2023 meeting.

Welcome to the eighth market scan from the IAASB's Disruptive Technology team. Building on our ongoing work, we issue Market Scans covering exciting trends, including new developments, corporate and start-up innovation, noteworthy investments and what it all might mean for the IAASB.

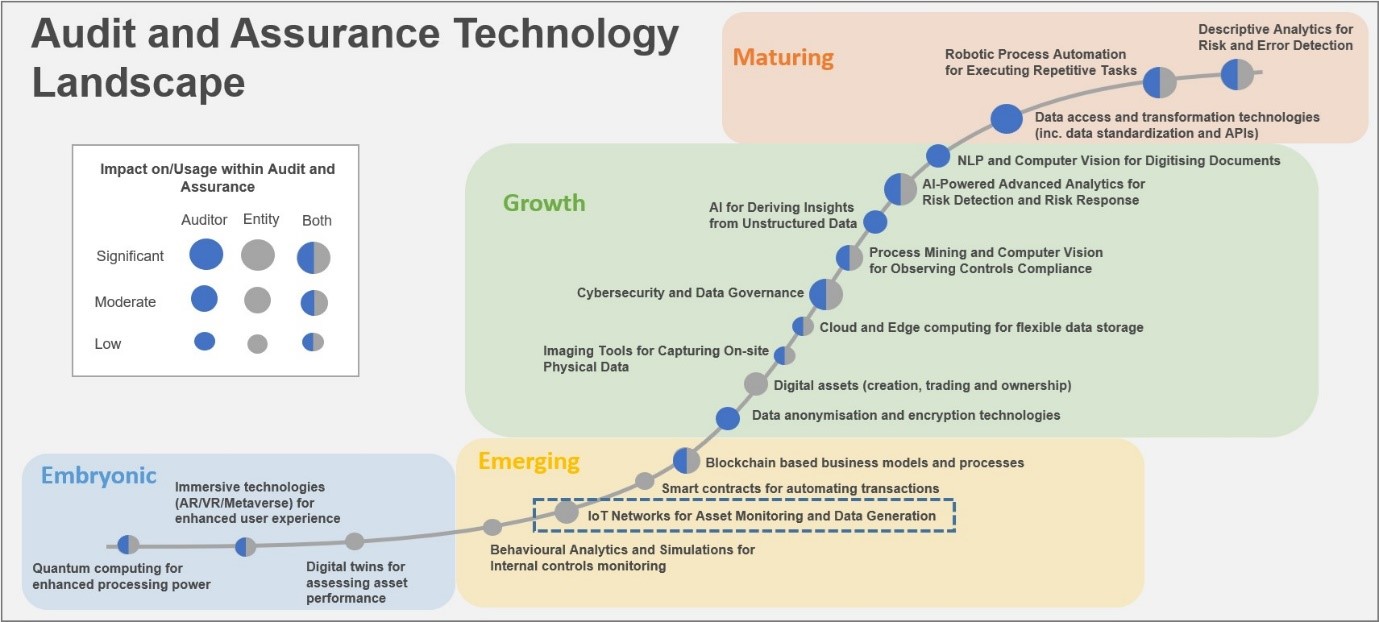

In this Market Scan, we explore the Internet of Things, focusing on Networks for Asset Monitoring and Data Generation, a technology that enables real time tracking, managing and monitoring of business processes and assets. It also may form part of an entity’s internal control system and may provide data inputs to non-financial reporting, such as emissions reporting.

We cover:

What is the Internet of Things? Why is it important?

The latest developments

What this might mean for the IAASB

What is the Internet of Things? Why is it important?

The Internet of Things (IoT) is a system of interconnected computing devices, mechanical and digital machines or devices in objects, animals, or people that are provided with unique identifiers and the ability to transfer data over a network without requiring human-to-human or human-to-computer interaction. IoT devices include consumer products, such as smart home and personal devices (e.g., Ring Doorbell, Apple Watch), and industrial products, such as medical monitoring applications or control sensors and systems used in transportation, manufacturing, and agriculture.

Digital Twin is a digital representation of a physical entity, such as an asset, process, system, device or even a person, and is an emerging technology related to the Internet of Things. This technology, coupled with other technologies, like artificial intelligence, machine learning or process mining, can be used to drive business and operational process efficiencies. For example, a digital twin of a wind turbine can be used to simulate component wear and tear in order to predict turbine performance and make assessments of optimal maintenance strategies and return on investment expectations.

What is IoT? | IoT - Internet of Things | IoT Explained in 6 Minutes | How IoT Works? | Simplilearn

The commercial benefits associated with deploying IoT technology include:

There are some challenges associated with these technologies, such as managing and maintaining all the devices in the network and ensuring the network operates securely, as well as safeguarding data quality and governance. The growth in IoT system complexity has given rise to IoT system management innovations to manage both internal device needs, such as software updates, as well as how those devices communicate across an IoT network. This may be done using a combination of interconnected information systems, for example, as shown in the diagram below.

From an audit and assurance perspective the implications related to an entity’s use of IoT devices and systems broadly are twofold. Firstly, these technologies may form part of the entity’s internal control system and, therefore, require consideration when identifying and assessing risks of material misstatement, including considerations around cybersecurity risks. Secondly, the data generated and collected may be used within the entity’s financial or non-financial reporting, such as sustainability-related disclosures and commentary, which warrants the auditor or assurance practitioner’s consideration of information intended to be used as evidence and the design and performance of audit/assurance procedures.

Recent Noteworthy Developments in Internet of Things

This section is designed to provide examples of recent developments that may signal future disruption in this area. It is not a complete list of all activities related to the IoT.

1. NIST selects ‘Lightweight Cryptography’ Algorithms to Protect Small Devices

In February 2023, the US National Institute of Standards and Technology (NIST) announced it had selected ASCON as having the winning bid for the "lightweight cryptography" program to find the best algorithm to protect small IoT devices with limited hardware resources.

In the announcement, NIST said, "The algorithm ensures that all of the protected data is authentic and has not changed in transit. AEAD [authenticated encryption with associated data] can be used in vehicle-to-vehicle communications, and it also can help prevent counterfeiting of messages exchanged with the radio frequency identification (RFID) tags that often help track packages in warehouses."

2. Start-up activity related to IoT systems and associated technologies

In May 2022, sustainability platform Sustain.Life raised USD $16m in seed funding to support its hiring, software development and customer growth. The platform is designed to help small- and medium-sized entities measure and report their carbon emissions and environmental impact.

In January 2023, Memfault, a platform that enables IoT device monitoring and maintenance over the cloud, secured USD $24m in Series B funding to expand its platform’s software support and invest in out-of-the-box integrations.

In January 2023, Forward Networks Inc, a US-based start-up, raised USD $50m in a Series D funding round to enable it to grow its digital twin technology. The technology creates “mathematically accurate digital twin models for sprawling enterprise networks that can drive actionable insights”.

What this might mean for the IAASB

The IAASB is interested in maintaining its collective knowledgebase on digital technologies (including on specific sub-topics such as the IoT), promoting digital readiness and enablement through its engagement with stakeholders, and encouraging action by others to supplement and support the IAASB’s standard-setting activities.

Subject to the IAASB’s work plan decisions, possible digital technologies use cases for audited entities, and audit or assurance engagements might provide input for further modernizing the IAASB’s standards to be adaptable to and reflect the current business and audit environment, while remaining principles based.

When deployed by entities, IoT devices and networks have the potential to create increased complexity in information systems due to the volume of interconnected devices that require appropriate consideration by the auditor when performing risk identification and assessment procedures. As this technology becomes more sophisticated, particularly where coupled with artificial intelligence technology, it may present novel risks, for example, where real-time analysis and refinement of the device occurs. This may present new challenges for the auditor and may, therefore, have implications for the IAASB’s work, whether in terms of future standard setting related to technology or facilitating or supporting action by others (e.g., developing guidance).

Regarding non-financial information assurance, audited entities are beginning to develop and implement technologies such as smart sensors to measure individual product’s carbon emissions as they move through the supply chain to gather data to measure carbon footprint. Assurance providers will need to develop approaches to evaluate the relevance and reliability of such information from IoT devices intended to be used as evidence and how the nature and source of this information affect the design and performance of procedures for identified disclosures of non-financial information.

The IAASB is currently working on a project to develop an overarching standard for assurance on sustainability reporting as a global baseline for sustainability assurance engagements, while anticipating the need to develop further standards as part of a suite of standards for sustainability assurance. Providing more specificity in relation to the implications of technology, such as the entity’s use of IoT technology and the assurance provider’s use of information produced from IoT sources, may prompt certain candidate topics for future standard-setting activities.

The growing reliance on IoT devices has created an unintended consequence for consumers, with large volumes of IoT devices no longer supported by their manufacturers. This has led to issues around security and waste, which are discussed in this article

Image

Caption

IAASB Audit & Assurance Technology Landscape, September 2022

The first IPSASB meeting of the year was hosted in the offices of the International Monetary Fund in Washington, D.C., USA on March 14-16, 2023.

Measurement

The IPSASB approved IPSAS 46, Measurement, which brings measurement guidance together in a single standard, and introduces a public sector specific current value measurement basis for assets held for their operational capacity and provides additional generic guidance on fair value. This completes the initial phase of the measurement project, now the IPSASB will consider the broader impact of this new guidance across IPSAS in the ongoing Measurement – Application Phase project.

IPSAS 46 will be effective for periods beginning on or after January 1, 2025.

Revenue

The IPSASB approved IPSAS 47, Revenue, which is a single standard to account for revenue transactions in the public sector. IPSAS 47 replaces the existing three revenue standards, and presents accounting models which will improve financial reporting and support effective public sector financial management.

IPSAS 47 will be effective for periods beginning on or after January 1, 2026.

Transfer Expenses

The IPSASB approved IPSAS 48, Transfer Expenses, which provides guidance on a major area of expenditure for governments and other public sector entities. IPSAS 48 fills a gap which had previously led to ambiguity and inconsistency of accounting policies in the public sector.

IPSAS 48 will be effective for periods beginning on or after January 1, 2026.

Reporting Sustainability Program Information

The IPSASB reviewed the responses to Exposure Draft (ED) 83, Reporting Sustainability Program Information–RPGs 1 and 3: Additional Non-Authoritative Guidance. The IPSASB considered the strong support from respondents on the ED 83 proposals, and approved Amendments to Recommended Practice Guideline 1, Reporting on the Long-Term Sustainability of an Entity’s Finances and Recommended Practice Guideline 3, Reporting Service Performance Information. These amendments help to highlight the applicability of existing concepts and principles in the respective RPGs which public sector entities can apply for reporting sustainability program information.

These amendments will be issued in the second quarter of 2023.

Sustainability Reporting

The IPSASB discussed findings from the initial research and scoping activities performed in Q1 2023. In light of current available resources, the IPSASB agreed to focus initially on a Climate-Related Disclosure project, as this was the most urgent issue identified in the feedback received to the Consultation Paper, Advancing Public Sector Sustainability Reporting.

The initial research and scoping activities will continue in Q2 2023 while the IPSASB continues to source incremental funds to support its sustainability standard setting.

Natural Resources

The IPSASB completed a first review of the responses to its Natural Resources Consultation Paper. The IPSASB agreed to develop an ED to propose accounting requirements for natural resources, including a principled approach to describing and identifying natural resources. The IPSASB also decided to develop a separate ED based on IFRS 6, Exploration for and Evaluation of Mineral Resources to introduce IPSAS guidance on accounting for the costs incurred during exploration, evaluation, and extraction activities.

The IPSASB approved updated Chapter 5, Elements in Financial Statements, which introduces minor changes to the definition of an asset and a liability, and adds new guidance on a transfer of resources, unit of account and binding arrangements that are equally unperformed.

Chapter 5 will be issued in the second quarter of 2023.

The IPSASB reviewed responses to ED 81, Conceptual Framework Update: Chapter 3, Qualitative Characteristics. The IPSASB agreed to update the qualitative characteristic of faithful representation to discuss prudence, and added guidance to clarify that omitting, misstating or obscuring information are factors relevant to consider when making materiality judgments.

Retirement Benefit Plans

The IPSASB performed an initial review of the responses to ED 82, Retirement Benefit Plans. While the overall proposals in ED 82 were strongly supported by respondents, the IPSASB agreed to analyze further specific issues raised at its next meeting in June 2023.

Measurement – Application Phase

The IPSASB agreed which IPSAS are in the scope of the application phase of the Measurement project. The IPSASB also concluded that the applicability of current operational value should be evaluated at initial and subsequent measurements for each IPSAS in scope of the project.

The IPSASB’s Next Strategy and Work Program

The IPSASB discussed the development plan for its next Strategy and Work Program. The IPSASB considered the environmental differences between 2023 and when the 2019-2023 Strategy was developed. The IPSASB agreed its current strategy, and its delivery through five themes, continued to be relevant, however, needed to evolve to address changing stakeholder expectations. The IPSASB aims to approve a Consultation at its September 2023 meeting and is planning outreach during the consultation period in Q4 2023.

Next Meeting

The next meeting of the IPSASB will take place in June 2023 in Toronto, Canada. For more information, or to register as an observer, visit the IPSASB website.

Welcome to the seventh Market Scan from the IAASB's Disruptive Technology team. Building on our ongoing work, we will issue a Market Scan every 2-3 months. Market Scans cover exciting trends, including new developments, corporate and start-up innovation, noteworthy investments and what it all might mean for the IAASB.

In this Market Scan, we explore Digital Assets, with a focus on recent developments within the Cryptocurrency market and what it might mean for the audit and assurance ecosystem. Future Market Scans will build on this area by focusing on related technologies, such as blockchain and smart contracts.

Technology Landscape, September 2022

We cover:

What are digital assets and why are they important?

The latest developments

What this might mean for the IAASB

What Are Digital Assets and Why Are They Important?

A digital asset is anything that exists in digital form only, has or provides value, is identifiable and discoverable, and is associated with ownership or use rights. Types of digital asset include cryptocurrencies and non-fungible tokens (NFTs) as well as digital content like photos, audio files, videos, websites, presentations, spreadsheets, or text files.

Cryptocurrencies (or crypto-assets) such as Bitcoin, Ethereum and Solana use blockchain technology, a distributed ledger that is a computerized database using strong cryptography to secure transaction records, control the creation of additional coins, and verify the transfer of coin ownership. Using this decentralized approach eliminates the need for traditional intermediaries, such as banks, to enable funds to be transferred between two parties. Cryptocurrencies can be bought and sold using accounts with cryptocurrency exchange platforms (e.g., Coinbase, Crypto.com) or through a standalone digital wallet.

Stablecoins are a type of cryptocurrency whose value is pegged to that of another currency, commodity or financial instrument. Stablecoins seek to offer price stability by maintaining reserve assets as collateral or through algorithmic formulas designed to control supply. Examples of stablecoins include Tether, USD Coin and TerraUSD.

Cryptocurrency coins are native to their own blockchain (e.g., Ether on the Ethereum blockchain) and are mainly used for payments, investments and trading.

Cryptocurrency tokens have many uses, such as for buying products (transactional tokens), representing ownership (security tokens), conferring voting rights (governance tokens), accessing services (utility tokens) or supporting decentralized applications on the blockchain (platform tokens).

Coins vs Tokens: What’s the Difference? Three-minute watch, Coin Gecko

The advantages of cryptocurrencies include less expensive and faster money transfers and decentralized systems that are not reliant on a central intermediary. Disadvantages of cryptocurrencies include their price volatility, high energy consumption for mining activities (where proof of work is the consensus mechanism used to confirm values on the blockchain) and how easy it is to use crypto for criminal activities.

From an audit and assurance perspective, there is an ever-increasing likelihood that audited entities may be engaged in digital asset related activities, such as holding, transacting or using digital assets; facilitating trading of digital assets on customers’ behalf; or creating digital assets for sale or distribution to third parties. These activities may have unique risks of material misstatement that need to be understood and appropriately addressed as part of a financial statement audit. For example, where digital assets are held by third parties (such as trading platforms or other custodians), obtaining an understanding of the material custodial arrangements and relevant controls related to safeguarding and maintaining records of those assets may be appropriate.

In its Inspections Insights publication in November 2019, the Canadian Public Accountability Board noted certain recurring findings in its inspections of audit files of reporting issuers with activities in the crypto-asset sector. Areas for improvement included:

Obtaining an adequate understanding of audit risks when designing the audit approach;

Evaluating the reliability of information to be used as audit evidence obtained from crypto-exchanges and custodians, as well as from blockchains;

Obtaining sufficient evidence to support an entity’s ownership claims to self-custodied crypto-assets; and

Performing procedures in addition to vouching crypto-assets received to the blockchain, for entities engaged in crypto-asset mining activities.

A follow-up publication in August 2022, Auditing in the Crypto-Asset Sector, highlighted considerations for auditors when auditing the financial statements of reporting issuers that use custodians to safeguard their crypto-assets.

Recent Noteworthy Developments in Digital Assets

These recent developments may signal ongoing or future disruption in this area. It is not a complete list of all activities related to digital assets.

How Terra's UST and LUNA Imploded |Decrypt – In May 2022, Terra’s UST stablecoin and governance token LUNA collapsed, sending shockwaves through the cryptocurrency market and leading to the fall in price of Bitcoin and other cryptocurrencies as investors started to pull their investments. This in turn led to crypto hedge fund Three Arrows Capital falling into liquidation and affected cryptocurrency lenders, including Voyager Digital, Celsius Network and BlockFi, which all subsequently filed for bankruptcy protection.

The Global Digital Assets and Cryptocurrency Association, a global self-regulatory association for the digital asset and cryptocurrency industry published an open letter calling for agreement on a set of fundamental core principles for the industry, including appropriate customer protection, governance and risk management procedures.

2. Crypto audits under scrutiny

Crypto Exchanges’ A La Carte Approach To Audits A Recipe For Disaster | MSN – A Forbes survey of the world’s largest cryptocurrency exchanges highlighted that not all are subject to full financial statement audits. The article noted that, “depending on where they are based, cryptocurrency exchanges do not have to submit to audits. If they do, their financial statements can remain private or be shared only with regulators. This is in stark contrast to issuers of publicly traded securities in major developed markets whose accounts must be regularly audited and made public.”

SEC Increases Scrutiny of Audits of Cryptocurrency Companies | WSJ – In the wake of the FTX collapse, a number of cryptocurrency exchanges sought to reassure investors by providing transparency reports or proof of reserves information, some of which had been subject to agreed-upon procedures (AUP) reporting by an independent auditor. However, the US Securities and Exchange Commission (SEC) raised concerns about investors placing too much confidence on the reporting, which Paul Munter, the SEC’s chief accountant, said, “is not enough information for an investor to assess whether the company has sufficient assets to cover its liabilities.” Several audit firms have stopped providing proof-of-reserves work in light of concerns over investor overreliance and reputational risk.

What This Might Mean for the IAASB

The IAASB is interested in maintaining its collective knowledgebase on digital technologies (including on specific sub-topics such as digital assets), promoting digital readiness and enablement through its engagement with stakeholders, and encouraging action by others to supplement and support the IAASB’s standard-setting activities.

Subject to the IAASB’s work plan decisions, possible digital technologies use cases for audited entities and audit or AUP engagements might provide input for further modernizing the IAASB’s standards so they are adaptable to and reflect the current business and audit environment, while remaining principles-based.

Despite the turbulence in the digital asset and cryptocurrency industry over the last year, there continues to be more than 300 million individual cryptocurrency users and approximately 18,000 businesses accepting crypto payments. The corporate failures experienced in this industry bring into focus audit’s important role in enhancing confidence in financial statements, thereby contributing to capital markets’ effective functioning and stability. In addition, it highlights the need for a consistent approach to financial reporting by, and regulation of, entities in the industry. Building suitable skills and expertise in this increasingly complex area is also necessary to enable audit and assurance professionals to act appropriately.

As this space evolves, the IAASB may need to consider how best to highlight the application of its principles-based standards in providing audit, assurance or related services to businesses operating in the digital asset ecosystem, including facilitating and supporting actions by others (e.g., in developing non-authoritative guidance).

British rock band Muse released their ninth studio album, Will of the People, in NFT form in August 2022 and it became the first NFT album to reach number 1 in the music charts.

The IPSASB held its second meeting of the year in New York on June 21-24, 2022.

Transfer Expenses

The IPSASB made significant progress in finalizing its transfer expense model. The IPSASB confirmed that a transfer provider’s enforceable rights in a binding arrangement is an asset that is derecognized as the rights are extinguished. For transfers without binding arrangements, the board decided the transfer expense is recognized when control of the transferred resources is lost.

Revenue

With the revenue accounting models largely shaped in 2021, the IPSASB focused on the application to public sector specific issues. The IPSASB confirmed that existing proposals related to the subsequent measurement of non-contractual receivables and disclosure requirements remain appropriate from a principled perspective. The board also confirmed that accounting principles for binding arrangements should be applied to account for capital transfers.

Measurement

After analyzing the additional information and perspectives from respondents, the IPSASB agreed to continue developing its public sector measurement basis, Current Operational Value (COV), for assets held for their operational capacity. The IPSASB confirmed the core principles of COV and agreed they should be clarified to enhance understandability. With the core principles agreed, the IPSASB will next focus their attention on developing the non-authoritative text to ensure clarity in their intended application in practice.

Conceptual Framework – Phase I

The IPSASB continued its analysis of assumption price, cost of release and net selling price. The IPSASB considered the approach of the International Accounting Standards Board and the broader relevance of these measurement bases to public sector financial reporting and decided not to include these measurement bases in a revised chapter on measurement.

Other Lease–Type Arrangements

The IPSASB agreed on the accounting for concessionary leases. For lessees, the IPSASB agreed to measure the right-of-use asset at fair value on initial recognition. For lessors, the IPSASB decided that the current IPSAS guidance is appropriate for concessionary leases.

ED 78, Property, Plant, and Equipment

The IPSASB performed a detailed review of the responses to ED 78, Property, Plant, and Equipment. The proposals in ED 78 were strongly supported by respondents. The IPSASB agreed to move forward with the proposals related to the structure of the guidance, characteristics of infrastructure assets, additional disclosure of unrecognized heritage assets, and non-authoritative guidance.

The IPSASB agreed to proposerevised definitions for an asset and a liability for inclusionin the Exposure Draft planned for approval in December 2020.

The IPSASB agreed to add obscuring information to theexisting factors influencing materiality—omissions and misstatements. The IPSASB also agreed to insert a new section on unit of account. Staff will carry out further work on the case for addressing executorycontracts explicitlyin the Framework.

Revenue and Transfer Expenses

The IPSASB clarified principles related to the existence and recognition of liabilities and assets in transactions arising with binding arrangements (in revenue and transfer expenses respectively). The IPSASB reconsidered and concluded that the distinction between transfer expenses with and without performance obligations is not useful from the transfer provider perspective.

Draft guidance in both standards will be revised to first require an entity to assess whether a binding arrangement exists, and clarify the scope of the proposed transfer expenses standard.

Natural Resources

The IPSASB reviewed the draft Consultation Paper(CP) and considered the proposals on the presentation of information on natural resources. The IPSASB also reviewed the revised chapters on living resources and water, as well as other miscellaneous changes to the CP. The IPSASB plans to continue development of the CP at its December 2020 meeting, with an aim to approve it at its March 2022 meeting.

Leases

The IPSASB decided to proceed with the proposals from Exposure Draft 75, Leases, including reconfirming those related to COVID-19 requirements, definition of a lease, lessee’s discount rate, and fair value definition. Further, the IPSASB decided that it will continue development of the leases guidance at its October check-in meeting with a plan to approve the new final Standard at its December meeting.

Accounting and Reporting by Retirement Benefit Plans

The IPSASB decided that the title for the standard being developed through this project should be Retirement Benefit Plans.The IPSASB also reviewed the options in IAS 26 and decided thatto provide better information and improve accountability and transparency, some of the options should be removed from the Exposure Draft under development. These options relate to the measurement and presentation of the actuarial present value of promised retirement benefits, and the valuation of plan assets.

Next Meeting

The next full-meeting of the IPSASB will take place virtually in December, 2021. For more information, or to register as an observer, visit the IPSASB website (www.ipsasb.org)

The IPSASB held its first meeting of the year virtually on March 16-19 and 23, 2021.

Accounting and Reporting by Retirement Benefit Plans

The IPSASB approved a Project Brief on Accounting and Reporting by Retirement Benefit Plans. In adapting IAS 26, Accounting and Reporting by Retirement Benefit Plans to the public sector, the IPSASB agreed to consider alternatives developed by National Public Sector Standard Setters to address the public sector issues identified.

IFRS 8, Operating Segments

The IPSASB received an educational session on a proposed limited-scope project to develop an IPSAS aligned with IFRS 8, Operating Segments. The session provided an overview of the requirements of IPSAS 18, Segment Reporting, IFRS 8, and public sector specific issues identified by stakeholders. The IPSASB decided to undertake more research and specifically gather further information related to the challenges in applying IPSAS 18 in practice before it decides whether to add the project to the Work Program.

Revenue

The IPSASB discussed several key topics arising from the responses received on the revenue Exposure Drafts (ED) 70 and ED 71. The IPSASB:

Decided that the proposed standards should be named and presented to reflect the prevalence of different types of revenue transactions in the public sector; and

Clarified the accounting principles related to the concepts of binding arrangements, performance obligations, and what gives rise to a liability in a binding arrangement without performance obligations.

Natural Resources

The IPSASB continued its review of the draft Consultation Paper (CP) and provided feedback on the measurement of subsoil resources, the approach used to draft the chapter on living resources, and the description of living resources. In addition, the IPSASB decided the CP will:

Include guidance on the costs of exploration, evaluation, development, and production activities;

Provide potential options on how this guidance could be incorporated into IPSAS literature; and

Solicit constituents’ views on these options.

Mid-Period Work Program Consultation

The IPSASB received presentations on its 2019-2023 Strategy and Work Plan and academic outreach initiatives, including three research papers on proposed projects. These presentations set the stage for a robust discussion on prioritizing projects to be proposed in the Mid-Period Work Program Consultation. The work to develop the Mid-Period Work Program Consultation will continue during Q2 2021, and it is expected to be approved in June 2021.

Conceptual Framework-Limited Update-Next Stage

The IPSASB agreed to the grouping of topics proposed for the next stage of the project. The topics are those in the original project brief not addressed in the first stage of the project, except for concepts of capital and capital maintenance, which, because of their complexity, should be taken forward separately on a longer timeframe. The IPSASB also agreed to add the description of service potential in the context of an asset to the list of topics.

Next Meeting

The next full-meeting of the IPSASB will take place virtually in June 2021. For more information, or to register as an observer, visit the IPSASB website.

The IPSASB held its fourth meeting of the year virtually on December 1-2;8-11; and 15, 2020.

ED 77, Measurement

The IPSASB voted to preliminary approve ED 77, Measurement. ED 77 provides detailed guidance on the implementation of commonly used measurement bases, including historical cost, current operational value, fair value and cost of fulfillment, and the circumstances under which these measurement bases are expected to be used. The IPSASB will finalize ED 77 at its February 2021 meeting.

ED 76, Conceptual Framework - Limited Scope Update

The IPSASB voted to preliminary approve ED 76, Conceptual Framework – Limited Scope Update. ED 76 updates Chapter 7 of the IPSASB’s Conceptual Framework to align with measurement in IPSAS, reflect experience in use of the Framework since publication in 2014, and post-2014 developments in the International Accounting Standards Board. The IPSASB will finalize ED 76 at its February 2021 meeting.

ED 78, Property, Plant, and Equipment

The IPSASB voted to preliminary approve ED 78, Property, Plant, and Equipment, which will replace the requirements in IPSAS 17, Property, Plant, and Equipment. ED 78 updates the accounting principles drawn from IPSAS 17 and proposes additional guidance related to the:

Measurement project by bringing in guidance on public sector specific measurement concepts.

Heritage project by adding accounting requirements for heritage assets.

Infrastructure project by introducing clarifications related to the accounting for infrastructure assets.

ED 75, Leases

The IPSASB approved ED 75, Leases and the Request for Information, Concessionary Leases and Other Arrangements Similar to Leases for publication with a 4-month comment period. Both documents are planned for publication in January 2021.

Natural Resources

The IPSASB continued its discussions on the draft Consultation Paper (CP) and:

Considered advice from the Consultative Advisory Group (CAG) on sovereign powers and the asset recognition criteria;

Reviewed the draft CP chapter on subsoil resources and provided input on whether subsoil resources can be controlled prior to extraction and when such resources can be reliably measured; and

Discussed IFRS 6, Exploration for and Evaluation of Mineral Resources and its potential applicability in the public sector.

Revenue & Transfer Expenses - ED 70-72

The staff presented the IPSASB with a preliminary analysis of the responses to Exposure Drafts (ED) 70-72, along with feedback from the December 2020 CAG meeting on the issues of the interrelation of the EDs and the extent of disclosures. The IPSASB provided feedback and further items for consideration at the March 2021 meeting, when staff will also provide further analysis on the responses received to the EDs, as well as a project management plan.

Next Meeting

The IPSASB will hold a virtual check-in meeting in February 2021 and hold its next full meeting in March, 2021. For more information, or to register as an observer for either meeting, visit the IPSASB website.

The IPSASB held its first ever virtual meeting on June 4, June 23-26 and June 30, 2020. This was the second IPSASB meeting of 2020.

Conceptual Framework - Limited Scope Review

The IPSASB approved a measurement hierarchy distinguishing Measurement Models, Measurement Bases and Measurement Techniques.

Historical Cost, Fair Value, Current Cost and Fulfillment Value (or Cost of Fulfillment) will be defined as bases.

Market Value and Replacement Cost will be defined as techniques.

The IPSASB will consider additional bases, including Value in Use and Cost of Release, in September. The selection of measurement bases will be linked to the Framework’s measurement objective.

Measurement

The IPSASB considered issues raised by constituents related to measurement bases identified in the Measurement Consultation Paper (CP). These foundational discussions, along with those in the related Conceptual Framework project, will shape the draft Measurement Exposure Draft (ED) that will be reviewed in September.

The IPSASB also discussed the impact of applying the CP Measurement definition of fair value across IPSAS and concluded that no change in terminology is required for the majority of IPSAS where the term fair value is currently applied.

Infrastructure

The IPSASB agreed “networks or systems” and “long useful lives” should be included as characteristics of Infrastructure Assets in IPSAS 17, Property, Plant and Equipment. These characteristics distinguish Infrastructure Assets from general property, plant, and equipment and present complexities in the application and implementation of existing principles in the Standard. Illustrative Examples and/or Implementation Guidance will be developed for September 2020 to help provide clarity.

Heritage

The IPSASB agreed “irreplaceable,” “restrictions,” and “long and sometimes unspecified useful lives” should be included as characteristics of Heritage Assets in IPSAS 17. These characteristics distinguish Heritage Assets from other property, plant, and equipment and present complexities in the application and implementation of existing principles in the Standard.

The IPSASB also approved the removal of the heritage assets scope exclusion from IPSAS 17.

Accounting for Non-Current Assets Held for Sale and Discontinued Operations

The IPSASB approved the Project Brief for the project to develop a standard aligned with IFRS 5, Accounting for Non-current Assets Held for Sale and Discontinued Operations. The IPSASB also agreed to add additional public sector disclosure requirements on the fair value of assets classified as held for sale to enhance transparency and accountability.

Leases

The IPSASB reviewed the draft Basis for Conclusion related to the history of the Leases project. The IPSASB decided to align with IFRS 16, Leases in the development of Exposure Draft on Leases. However, it also decided to exclude the IFRS 16 manufacturer or dealer lessor requirements because these are not expected to be applicable in the public sector. The IPSASB considered the structure and content of the Request for Information that will be developed for publication together with the Exposure Draft on Leases to gather information on transactions and arrangements similar to leases.

Next Meeting

The next meeting of the IPSASB will take place in September, 2020. For more information, or to register as an observer, visit the IPSASB website (www.ipsasb.org).

The IPSASB held its first meeting of 2020 from March 10-13, 2020 at the IFAC offices in New York, USA.

Infrastructure Assets

The IPSASB decided that infrastructure assets are a subset of property, plant and equipment and considered the characteristics which differentiate them. The IPSASB will agree the infrastructure assets characteristics after analyzing the remaining issues. The IPSASB also considered the issues of depreciation, spare parts and dismantling costs. The IPSASB will continue these discussions at its June meeting. Access Presentation >>

Heritage

The IPSASB considered whether heritage items are resources and controlled for financial reporting purposes. The IPSASB decided that tangible heritage items are assets when they meet the definition of property, plant and equipment and concluded they should be depreciated and tested for impairment, except under certain specific circumstances.

Revised guidance related to these issues will be developed for the IPSASB’s consideration at its June meeting. Access Presentation >>

Measurement

The IPSASB reviewed the responses to the Measurement Consultation Paper. The IPSASB agreed that the existing accounting policy choice in IPSAS 5, Borrowing Costs, which allows borrowing costs that are directly attributed to qualifying assets to be either expensed as incurred or capitalized, should be retained. Additional guidance will be developed for the IPSASB’s consideration at its June meeting.

The IPSASB identified several themes in its review of the responses and will further address these during its June and September meetings. Access Presentation >>

Conceptual Framework - Limited Scope Update

The IPSASB approved a project brief on the Limited Scope Update of the Conceptual Framework (the Framework) subject to minor drafting and editorial changes. The project addresses specified issues identified from the IPSASB’s experience in using the Framework, as well as considering relevant developments in the finalized Conceptual Framework of the International Accounting Standards Board, which was published in March 2018. It is not an extensive review.

The IPSASB approved a project brief on Natural Resources subject to minor drafting and editorial changes. The first part of this project will develop a comprehensive consultation paper covering the recognition, measurement, and disclosure of subsoil resources, living resources and water. Access Presentation >>

Leases

The IPSASB decided to continue the project in phases, firstly, by developing an ED based on IFRS 16, followed by a second phase addressing the accounting for concessionary leases, which is a prevalent public sector issue. The IPSASB also agreed that the exposure draft based on IFRS 16 should request constituent input on concessionary leases to help with the second phase of the project. Access Presentation >>

Accounting for Non-Current Assets Held for Sale and Discontinued Operations in the Public Sector

The Board reviewed a proposal for a project to align with IFRS 5, Non-current Assets Held for Sale and Discontinued Operations. The IPSASB agreed that the project should proceed and identified public sector issues for further consideration. The IPSASB also recommended that the project be discussed with the Consultative Advisory Group at its June 2020 meeting. It will then be discussed with the IPSASB at its June 2020 meeting. Access Presentation >>

Meeting Podcast

A podcast highlighting key points of the March 2020 meeting is now available here.

Next Meeting

The next meeting of the IPSASB will be in Toronto, Canada from June 23-26, 2020 with the Consultative Advisory Group Meeting on June 22, 2020. For more information, or to register as an observer, visit the IPSASB website.