The International Public Sector Accounting Standards Board’s (IPSASB) Strategy and Work Plan 2024-2028 includes alignment with Government Finance Statistics[1] (GFS) as an integral part of the Board’s work.

The IPSASB’s Policy Paper Process for Considering GFS Reporting Guidelines During Development of IPSASs sets out the IPSASB process for considering GFS reporting guidelines during the development of IPSAS in order to reduce unnecessary differences with International Public Sector Accounting Standards (IPSAS Accounting Standards).

Although IPSAS Accounting Standards and ISS have different objectives and treat some transactions and events differently, they also have many similarities, such as the accrual-based accounting system, the reporting of assets, liabilities, revenues, and expenses, and the notion of control.

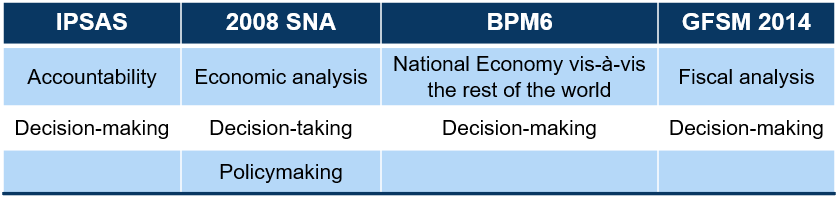

Table 1 – Objectives of IPSAS Accounting Standards and ISS

Often, IPSAS-based financial statements and ISS reports share the same users, so confusion arises as a result of the existence of differences between the two types of financial information.

The existence and extent of similarities between IPSAS Accounting Standards and ISS makes a strong case for direct usage of IPSAS-based financial information for statistical compilation and to reduce unnecessary differences between IPSAS Accounting Standards and ISS.

The main benefits of IPSAS Accounting Standards and ISS alignment are:

- Better quality of macroeconomic information—using the IPSAS-based financial information directly from the audited financial accounts reduces the need for surveys and statistical extrapolations.

- Better information for decision-making through more consistent understanding of the economic reality that both accounting systems aim to represent—enhances the linkages between the microeconomy and the macroeconomy.

- Reduced workload and avoidance of duplication of work for statistical compilers in obtaining source data for statistical compilation where the source data already exists in IPSAS reports.

The IPSAS Standards-GFSM Alignment Dashboard provides an overview of the differences between both accounting systems and updated status of relevant issues being considered in the update of ISS. For more details, see the IPSASB's project page on ISS.

[1] The overarching standards for macroeconomic statistics are set out in the System of National Accounts 2008 (2008 SNA). International statistical standards (ISS) are harmonized with the 2008 SNA to the extent possible, while remaining consistent with their own specific objectives. ISS include the European System of Accounts 2010 (2010 ESA), International Monetary Fund’s (IMF) Government Finance Statistics Manual 2014 (GFSM 2014), and Balance of Payments and International Investment Position Manual (Sixth Edition).